Many suppliers and manufacturers still evaluate distributor credit requests through manual credit review processes. Credit teams assess distributor profiles, review historical payment behavior, examine financial statements, and determine the appropriate credit limit that can be extended to the business customer.

While this approach provides human oversight, it also introduces operational complexity. Decision criteria may be applied differently across teams, policy updates take time to implement across workflows, and reviewing large numbers of applications often requires additional coordination between risk teams, credit officers, and lending operations.

Credit decisioning software helps bring structure to this process. These platforms evaluate applicant data against defined credit rules, integrate risk scoring models, document decision logic, and generate approval or review outcomes within a consistent framework.

This article walks through how credit decisioning software operates in lending workflows, the capabilities these systems provide, how they support credit risk evaluation, and the factors lenders should examine when selecting a platform.

Understanding Credit Decisioning Software

Credit decisioning software is a system used by businesses to evaluate credit applications using predefined decision rules and risk models. Instead of relying entirely on manual underwriting, the platform assesses applicant information within a structured decision engine.

When a credit application enters the system, relevant data is collected and evaluated against credit policies configured by the lender. These policies determine how the system interprets risk signals and what outcomes should follow when specific conditions are met.

Since the decision logic is defined within the platform, lenders can implement policy updates more easily, apply the same evaluation standards across applications, maintain a clear record of decision reasoning, and support regulatory audits when required.

How Credit Decisioning Software Works in 4 Steps

Credit decisioning software evaluates a credit application by passing it through a defined sequence of checks. Each stage examines specific information and determines how the application should move forward.

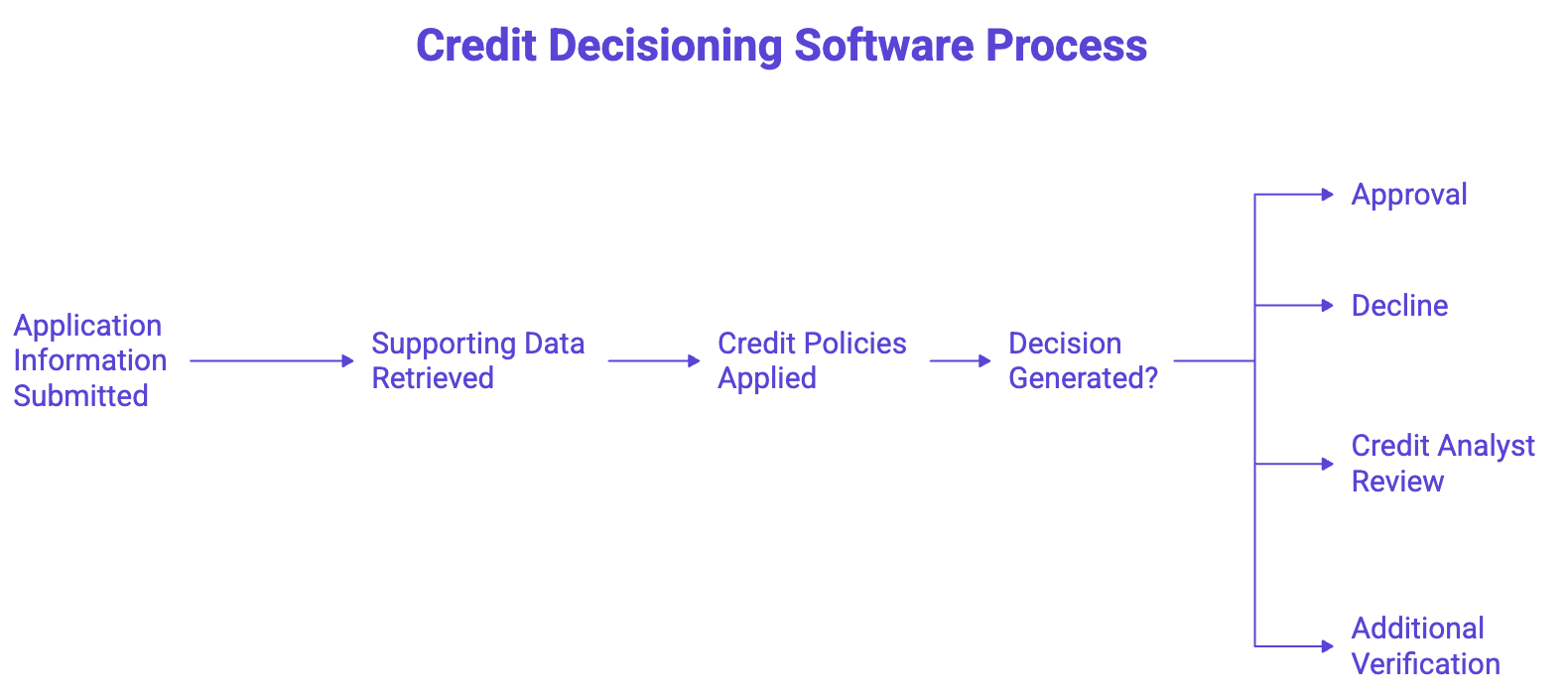

Step 1: Application Information Is Submitted

The process begins when a borrower submits a credit application through a lender’s website, mobile app, or lending portal. The system captures the applicant’s details and stores them for evaluation.

For example, an online loan form may collect the applicant’s name, income details, employment information, and the amount of credit requested.

Step 2: Supporting Data Is Retrieved

After the application is received, the system gathers additional information required for assessment. This often includes credit bureau reports, identity verification results, fraud-screening outcomes, internal customer records, and transaction history if the applicant is already a customer.

For instance, the system may retrieve a credit score from a bureau, confirm identity using a verification service, and check whether the applicant already holds an active loan with the institution.

Step 3: Credit Policies Are Applied

The software then checks the application against the lender’s credit policies. These policies define eligibility requirements, acceptable credit score ranges, income thresholds, debt-to-income limits, and rules that determine whether an application qualifies for further processing.

For example, a policy may require a minimum credit score of 680, stable employment history, income above a defined threshold, and no recent loan defaults.

Step 4: A Decision Is Generated

After the checks are completed, the system determines the next action. The application may move forward for approval, be declined based on policy conditions, be routed to a credit analyst for further review, or be placed on hold if additional verification is required.

For example, an application with strong credit indicators may be approved automatically, while one that triggers a policy exception may be flagged for manual review.

Each stage follows the policies defined by the lender, allowing applications to be evaluated in a consistent and traceable manner.

Benefits of Credit Decisioning Software for Businesses

When credit evaluations are supported by a structured decisioning system, businesses can apply policies more consistently, process applications with fewer manual dependencies, adjust credit rules more easily, and maintain clearer records of how decisions were made.

Improved Consistency in Credit Evaluations

When credit policies are defined within a decisioning platform, applications are assessed using the same evaluation criteria. This reduces variation that may occur when different analysts interpret policies differently. For example, if a lending policy requires a minimum credit score and a defined income threshold, those conditions are applied uniformly to every applicant.

Faster Credit Application Processing

Credit decisioning software retrieves required data automatically and evaluates the application once the necessary information becomes available. For instance, once bureau data and identity verification results are received, the system can complete the evaluation without waiting for manual review.

Easier Credit Policy Updates

Lending institutions periodically revise their credit policies to reflect updated risk strategies or regulatory requirements. Decisioning platforms allow these rules to be modified directly within the system. For example, a lender may change credit score thresholds, introduce additional verification checks, add restrictions for recent delinquencies, or adjust limits for a specific loan product.

Clearer Documentation of Credit Decisions

Decisioning systems store the information used during evaluation, the policy conditions that were triggered, the risk indicators identified during assessment, and the outcome generated for the application. This documentation helps lenders review decisions and demonstrate how credit policies were applied during evaluation.

Factors to Consider When Choosing Credit Decisioning Software

Selecting a credit decisioning platform requires evaluating how the system will support credit policies, data access, and decision oversight within lending operations.

- Policy Configuration Flexibility: This documentation helps organizations review credit limit decisions for retailers or business customers and demonstrate how credit policies were applied during evaluation. Credit policies such as score thresholds, income requirements, eligibility criteria, and product limits should be adjustable directly within the system.

- Data Source Integration: The platform should support connections with credit bureaus, identity verification services, fraud screening tools, internal customer databases, and loan origination systems so required data can be accessed during application evaluation.

- Risk Model Compatibility: The system should support bureau scores, internally developed risk models, behavioral scoring frameworks, and product-level risk models used across different lending products.

- Decision Transparency and Auditability:Businesses must be able to review how credit decisions were produced. The platform should record the information evaluated during processing, the rules applied during evaluation, the risk indicators identified during assessment, and the outcome generated for the application.

Building a Clearer and More Reliable Credit Decision Process

Credit decisioning software gives suppliers a structured way to evaluate distributor credit requests and manage how credit limits are assigned to business customers. By bringing credit policies, distributor information, and decision records into a single system, organizations can apply credit rules more consistently across their customer base.

This article discussed how credit decisioning software works, the stages involved in evaluating distributor credit requests, the capabilities organizations should examine when selecting a platform, and the benefits these systems bring to trade credit management.

For suppliers and manufacturers reviewing their credit management processes, understanding these systems can help improve how distributor credit limits are evaluated, approved, and documented across business relationships.